Offences and penalties Under GST

Late Fees For Non Filing Or Late Filing Of Returns (Section 47) Any Registered person who :

a.Fails to furnish details of outward or inward supplies u/s 37 or 38 or 39 or 45 before the due date.b.Late fees : Rs. 100/- per day (Max of Rs. 5000/-)

Offences (Section 122 (1))

Section 122 (2)

Any registered person who supplies any goods or services or both on which any tax has not been paid or short paid or erroneously refunded or where ITC has been wrongly availed or utilized

Supplies any Goods or Services without issue of invoice (Issues incorrect or False Invoice) Issues invoice without supply of goods. Collects Tax but fails to pay it to the Government. Collects Tax in contravention of the act but fails to pay the same to the Government Fails to deduct tax Fails to collect tax Takes Input Tax Credit without actual receipt of goods or services Fraudulently obtains refund under this act. Takes or distributes ITC in contravention of the act. Falsifies or produces financial records or produces fake accounts. Is liable to be registered but fails to get registered. Furnishes any false particulars either at the time of registration or subsequently. Prevents any officer in discharge of his duties under this act. Transports any taxable goods without documents Suppresses his turnover. Fails to keep or maintain books of Accounts. Fails to furnish information or documents called for by an officer. Supplies transports or stores any goods which are liable to confiscation under this act. Issues any invoice by using registration No of another person. Tampers with or destroys any material evidence or document Disposes off or tampers with any goods that have been detained, seized or attached.

Rs. 10000/- An amount equivalent to the amount of tax evaded / not deducted / Collected or Input Tax Credit Availed or distributed or refund claimed in the matter.

Without a fraudulent intention. Higher of the following

Rs. 10000.0010% of the tax due

With a fraudulent intention. Higher of the following

Rs. 10000.00Tax due

Section 122 (3)

Any Person who :

Aids or abets any of the offences specified in clauses (i) to (xxi) of Sub Sec 1.Acquires possession of or conceals himself in transporting, depositing, keeping, concealing, supplying or purchasing goods which are liable to confiscation.Receives or is in any way concerned with the supply of services which are in contravention of this act.Fails to appear before the officer.Fails to issue invoice or fails to account for the an invoice in his books of accounts

Shall be liable to penalty which may extend upto Rs 25000.00

Section 123

Penalty for failure to furnish Information Return u/s 150 :Rs. 100/- for each day during which the failure to furnish such return continues

Section 124

If any person required to furnish any information u/s 151 (a) Without reasonable cause fails to furnish information or return. (B) Wilfully furnishes or causes to furnish any information or return which is false.

He shall be punishable with a fine which may extend to Rs. 10000/-Which may extend upto Rs. 100/- for each day during which the offence continues subject to a maximum of Rs. 25000/-

General Penalty (Sec 125)

Any person who contravenes the provisions of this Act.For which no penalty is prescribedPenalty – may extend upto Rs. 25000/-

General Disciplines Related To Penalty

No Penalty for Minor Breach of Tax Regulation or Procedural Requirement – Minor breach : amount of tax involved is less than Rs. 5000/-No Penalty for a mistake which is easily rectifiable. No penalty without following the principles of Natural Justice.The officer imposing penalty shall specify the nature of breach and the applicable law under which the amount of penalty has been specifiedVoluntary Disclosure of a breach: – The proper officer may consider this fact as a mitigating factor when quantifying for the penalty.The provisions of this section shall not be followed if penalty is fixed under this law.

Detention of Goods

Notwithstanding anything contained in this actWhere any person transports or stores any goods which are in contravention of the act.All such goods and the conveyance used to transport such goods shall be liable to detention or seizure.

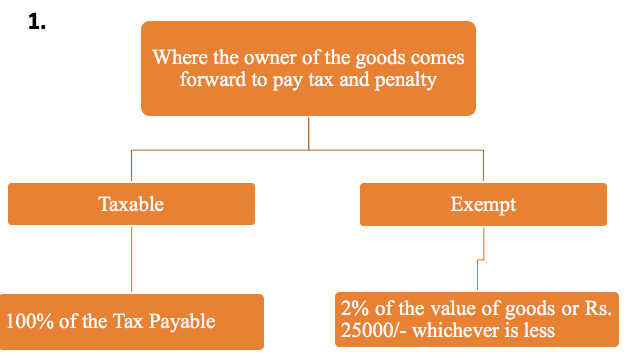

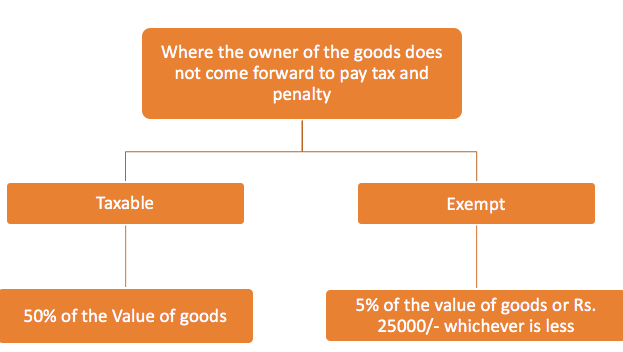

Release of Detained Goods

Confiscation of Goods (Section 130)

Supplies or receives any goods in contravention of this act with an intent to evade payment of tax.Does not account for any goods on which he is liable to pay tax under this act.Supplies any goods liable to tax under this act without getting registered.Contravenes any of the provisions of this Act with an intent to evade payment of tax.Uses any conveyance as a means of transport for carriage of goods in contravention of the act unless the owner of the conveyance proves that it was so used without knowledge or connivance of the owner

Fine in lieu of Confiscation

The Adjudging officer shall give an option to pay fine in lieu of confiscation.Such fine shall not exceed the market value of goods less tax chargeable thereon.Provided also, that where any such conveyance is used for the carriage of the goods, the owner of the conveyance shall be given an option to pay a fine equal to the tax payable on the goods being transported thereon in lieu of confiscation.

Why GST For IndiaRole of Chartered Accountants in GSTGST ObjectiveGST Current Tax StructureFiling of GST ReturnsWhen will GST be applicableList of Taxes Included in GSTImpact of GST in Indian EconomyGST RegistrationGST Rates

If you have any query or suggestion regarding “Offences and Penalties Under GST” then please tell us via below comment box….