1. What are payments to be made under GST?

Under GST the tax to be paid is mainly divided into 3 –

IGST – To be paid when interstate supply is made (paid to center)CGST – To be paid when making supply within the state (paid to center)SGST – To be paid when making supply within the state (paid to state)

Apart from the above payments a dealer is required to make these payments –

Tax Deducted at Source (TDS) – TDS is a mechanism by which tax is deducted by the dealer before making the payment to the supplier

For example – A government agency gives a road laying contract to a builder. The contract value is Rs 10 lakh. When the government agency makes payment to the builder TDS @ 1% (which amounts to Rs 10,000) will be deducted and balance amount will be paid.

Tax Collected at Source (TCS) – TCS is mainly for e-commerce aggregators. It means that any dealer selling through e-commerce will receive payment after deduction of TCS @ 2%.

This provision is currently relaxed and will not be applicable to notified by the government.

Reverse Charge – The liability of payment of tax shifts from the supplier of goods and services to the receiver. To know more about reverse charge check out our article ‘Know all about Reverse Charge under GSTInterest, Penalty, Fees and other payments

What are CPIN, CIN, BRN and E-FPB?

CPIN stands for Common portal Identification Number. It is created for every Challan successfully generated by the taxpayer. It is a 14-digit unique number to identify the challan. CPIN remains valid for a period of 15 days CIN or Challan Identification Number is generated by the banks, once payment in lieu of a generated Challan is successful. It is a 17-digit number that is 14-digit CPIN plus 3-digit Bank Code. CIN is generated by the authorized banks/Reserve Bank of India (RBI) when payment is actually received by such authorized banks or RBI and credited in the relevant government account held with them. It is an indication that the payment has been realized and credited to the appropriate government account. CIN is communicated by the authorized bank to taxpayer as well as to GSTN. BRN or Bank Reference Number is the transaction number given by the bank for a payment against a Challan E-FPB stands for Electronic Focal Point Branch. These are branches of authorized banks which are authorized to collect payment of GST. Each authorized bank will nominate only one branch as its E-FPB for pan India transaction. The E-FPB will have to open accounts under each major head for all governments. Any amount received by such E-FPB towards GST will be credited to the appropriate account held by such E-FPB. For NEFT/RTGS Transactions, RBI will act as E-FPB.

2. How to calculate the GST payments to be made?

Usually, the Input Tax Credit should be reduced from Outward Tax Liability to calculate the total GST payment to be made. TDS/TCS will be reduced from the total GST to arrive at the net payable figure. Interest & late fees (if any) will be added to arrive at the final amount. Also, ITC cannot be claimed on interest and late fees. Both Interest and late fees are required to be paid in cash. The way the calculation is to be done is different for different types of dealers – Regular Dealer A regular dealer is liable to pay GST on the outward supplies made and can also claim Input Tax Credit (ITC) on the purchases made by him. The GST payable by a regular dealer is the difference between the outward tax liability and the ITC. Composition Dealer The GST payment for a composition dealer is comparatively simpler. A dealer who has opted for composition scheme has to pay a fixed percentage of GST on the total outward supplies made. GST is to be paid based on the type of business of a composition dealer.

3. Who should make the payment?

These dealers are required to make GST payment –

A Registered dealer is required to make GST payment if GST liability exists.Registered dealer required to pay tax under Reverse Charge Mechanism (RCM).E-commerce operator is required to collect and pay TCSDealers required deducting TDS

4. When should GST payment be made?

GST payment is to be made when the GSTR 3 is filed i.e by 20th of the next month.

5. What are the electronic ledgers?

The Electronic Cash Ledger contains a summary of all the deposits/payments made by a taxpayer. Electronic Cash Ledger is maintained on the GST Portal. The Electronic Cash Ledger has to be maintained in prescribed form on the common portal by a person liable to pay tax.

6. How to make GST payment?

GST payment can be made in 2 ways –

Payment through Credit Ledger –

The credit of ITC can be taken by dealers for GST payment. The credit can be taken only for payment of Tax. Interest, penalty and late fees cannot be paid by utilizing ITC.

Payment through Cash Ledger –

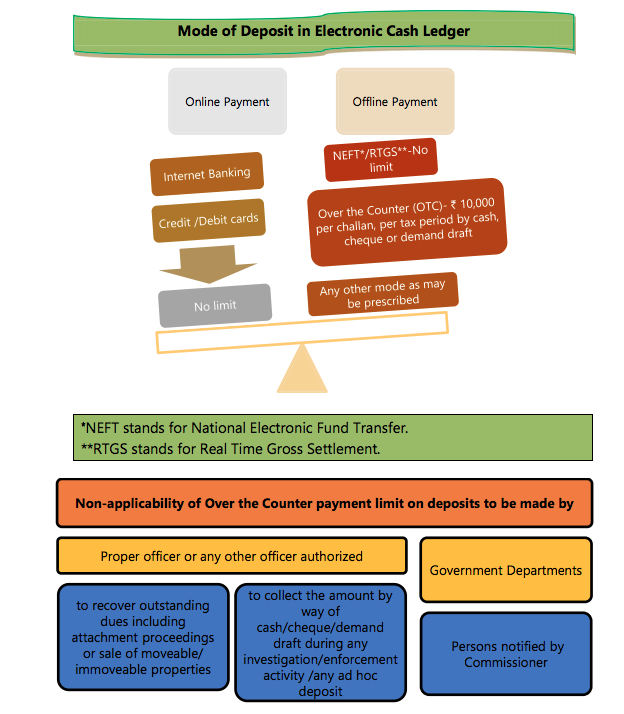

GST payment can be made online or offline. The challan has to be generated on GST Portal for both online and offline GST payment. Where tax liability is more than Rs 10,000, it is mandatory to pay taxes Online.

7. What is the penalty for non-payment or delayed payment?

If GST is short paid, unpaid or paid late interest at a rate of 18% is required to be paid by the dealer.Also, a penalty to be paid. The penalty is higher of Rs. 10,000 or 10% of the tax short paid or unpaid.