AS 20 Earning Per Share

Applicable to CFSPotential Equity Share is a Financial InstrumentExample of Potential Equity Share Convertible Debt instruments or preference shares into equity shares; Share warrants; Options – ESOP; and Contingently issuable shares Present basic and diluted EPS, even if the amounts disclosed are negative (loss per share).

Basic EPS = Net Profit After Tax (-) Preference Dividend [+ Tax on Divd] / Weighted Avg. No. of Equity Shares O/s during the Period

NPAT is After Prior Period Item & Extraordinary Item as per AS 5Does not include any preference dividends paid or declared during the current period in respect of previous periods.Weighted Avg. No. of Equity Shares O/s during the Period

Computation of Weighted Average: (1,800 X 12/12) + (600 X 7/12) – (300 X 2/12) = 2,100 shares.

Time Weighting Factor [Relevant Dates for Weight]

Partly paid shares are entitled to participate in the dividend to the extent of amount paid

Merger Nature of Purchase

Computation of weighted average would be as follows: (1,800×12/12) + ([600×5/10] x2/12) = 1,850 shares

If enterprise has more than one class of equity shares, net P/L is apportioned over the different classes of shares as per their dividend rights.Equity shares of different nominal values but with the same dividend rights = Number of equity shares is calculated by converting all such equity shares into equivalent number of shares of the same nominal value.Weighted average number of equity shares outstanding during the period and for all periods presented should be adjusted for events, that have changed the number of equity shares outstanding, without a corresponding change in resources [other than the conversion of potential equity shares].

⇓ Examples

Bonus issue;Bonus element in any other issue [Eg. Rights issue];Share split; andReverse share split (consolidation of shares).

Bonus Issue or Share Split

Issued to existing shareholders for no additional consideration. Number of shares outstanding is increased without increase in resources. Number of equity shares outstanding before the event – Adjusted as if the event had occurred at the beginning of the earliest period reported.

- Bonus Considered only for Calculating Adjusted EPS – Not for Basic EPS for Earlier Period

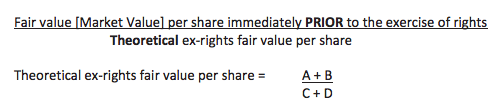

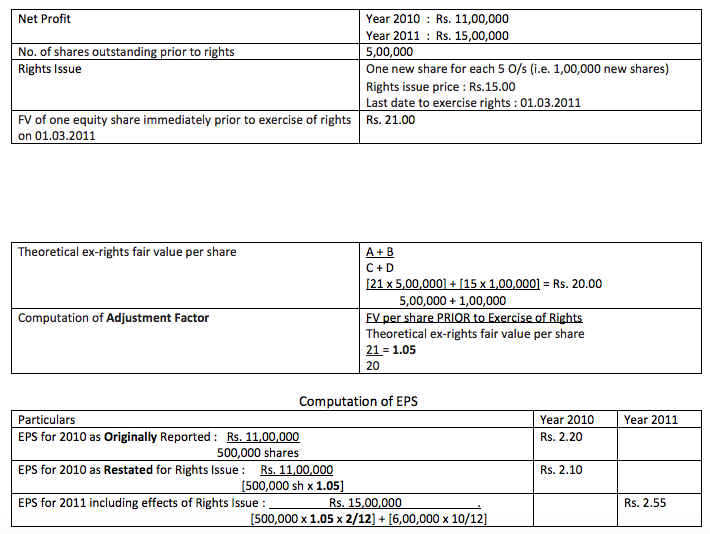

Rights Issue

Conversion of potential equity shares – No Bonus Element – issued for full valueIn Rights Issue – Exercise price less than fair value of shares – includes bonus elementNumber of equity shares used in calculating basic EPS for all periods PRIOR to rights issue is the number of equity shares outstanding prior to issue, multiplied by the following factor:

A = Fair Value [Market Price] of ALL Shares O/s Immediately BEFORE Exercise of Rights B = Total Amount Received From Exercise of Right C = No. of Shares Outstanding PRIOR to Rights Offer D = No. of Shares Issued in Exercise of Rights

Calculating Diluted EPS

Diluted EPS = Net Profit Available for Equity Shares [After Adjustment of Diluted Earnings] / Wtd. Avg. of Sh. O/s during the period [Assuming Conversion of diluted Potential Eq. Sh. [DPES]] Calculation of Diluted Earnings Addition in No. of Shares DPES should be deemed to have been converted into equity shares at the Beginning of the Period OR if issued Later, Date of Issue of PES. Share application money pending allotment or any advance share application money as at the balance sheet date, which is not statutorily required to be kept separately and is being utilised in the business of the enterprise, is treated in the same manner as DPES for the purpose of calculation of diluted EPS.

Contingently Issuable Shares [CIS]

Issuable upon satisfaction of certain conditions resulting from contractualIncluded in the computation of both BASIC EPS AND DILUTED EPS from the date when the conditions under a contract areIf conditions not met, for computing DILUTED EPS, CIS are included as of the beginning of the period or as of the date of contingent share agreement, if [If Conditions not met then do not include CIS in Basic EPS]Restatement is not permitted if conditions are not met when contingency period actually expires subsequent to the end of the reporting period. This provisions apply equally to PES that are issuable upon the satisfaction of certain conditions (contingently issuable PES).

Options and other share purchase arrangements Dilutive when they would result in the issue of equity shares for less than fair value.

Dilutive Potential Equity Shares

Dilutive when & only when, their conversion to equity shares would decrease net profit per share from continuing ordinary operations.Net profit per share from continuing ordinary operations.

Anti-dilutive when their conversion to equity shares would increase EPS or decrease loss per share. Effects of anti-dilutive potential equity shares are ignored in calculating diluted In order to maximise dilution of basic EPS, each series of potential equity shares is considered in sequence from the most dilutive to least dilutive.For determining the sequence = Earnings per incremental potential equity share is calculated.Where earnings per incremental share is the least, Potential equity share is considered most

Increase in Earnings Attributable to Equity Shareholders on Conversion of Potential Equity Shares Attributable tax, e.g., corporate dividend tax 10% Options are most dilutive as their earnings per incremental share is nil. Options will be considered first. 12% convertible debentures being second and convertible preference shares will be third. Conversion of Diluted Earnings Per Shares Diluted EPS increased when taking convertible preference shares (from 3.06 to 3.34) – Convertible preference shares are anti-dilutive and are ignored in calculating diluted EPS. Therefore, Diluted EPS is 3.06.

Potential equity shares that cancelled or allowed to lapse during the reporting period – included in computing diluted EPS only for the portion of the period during which they were outstanding.Potential equity shares that converted into equity shares during the reporting period – included in the calculating diluted EPS from the beginning of the period to the date of conversion;From the date of conversion, Resulting equity shares are included in computing both basic and diluted EPS.

RESTATEMENT

Calculation of basic and diluted EPS should be adjusted for all the periods presented.If changes occur after balance sheet date but before date when financial statements are approved by BOD – per share calculations adjusted for all the periods presented.Enterprise is encouraged to provide description of equity share transactions or potential equity share transactions, OTHER THAN – 1. Bonus Issue Share Split & 2. Reverse Share Split

Which occur after the balance sheet date. Examples of such transactions include :

Issue for cash;Issue to use proceeds to repay debt or preference shares outstanding at the balance sheet date;Cancellation of equity shares outstanding at the balance sheet date;Conversion of potential equity shares, outstanding at the balance sheet date;Issue of warrants, options or convertible securities; andSatisfaction of conditions that result in issue of contingently issuable shares

⇑ EPS not adjusted for such transactions occurring after balance sheet date because such transactions do not affect the amount of capital used to produce the net profit or loss for the period.Satisfaction of conditions that result in issue of contingently issuable shares. ⇓ Only Transaction Mentioned in Para 44 will be Adjusted About Author Jigz Vira Recommended Articles

Download Accounting Standard 22Accounting standard 2AS 1 Disclosure of Accounting PoliciesAccounting Standard 3AS 12 Accounting for Government GrantsAS 5 Net Profit or Loss for the PeriodAccounting Standard 15Accounting Standard 16

If you have any query or suggestion regarding “AS 20 Earning Per Share” then please tell us via below comment box….